Medicaid is a joint program with the federal government and is run by each state (the rules are generally similar but do vary by state).

Below is an example from the CLTC course (a 600+ page textbook to pass the test) to earn the “Certified in Long-Term Care” designation.

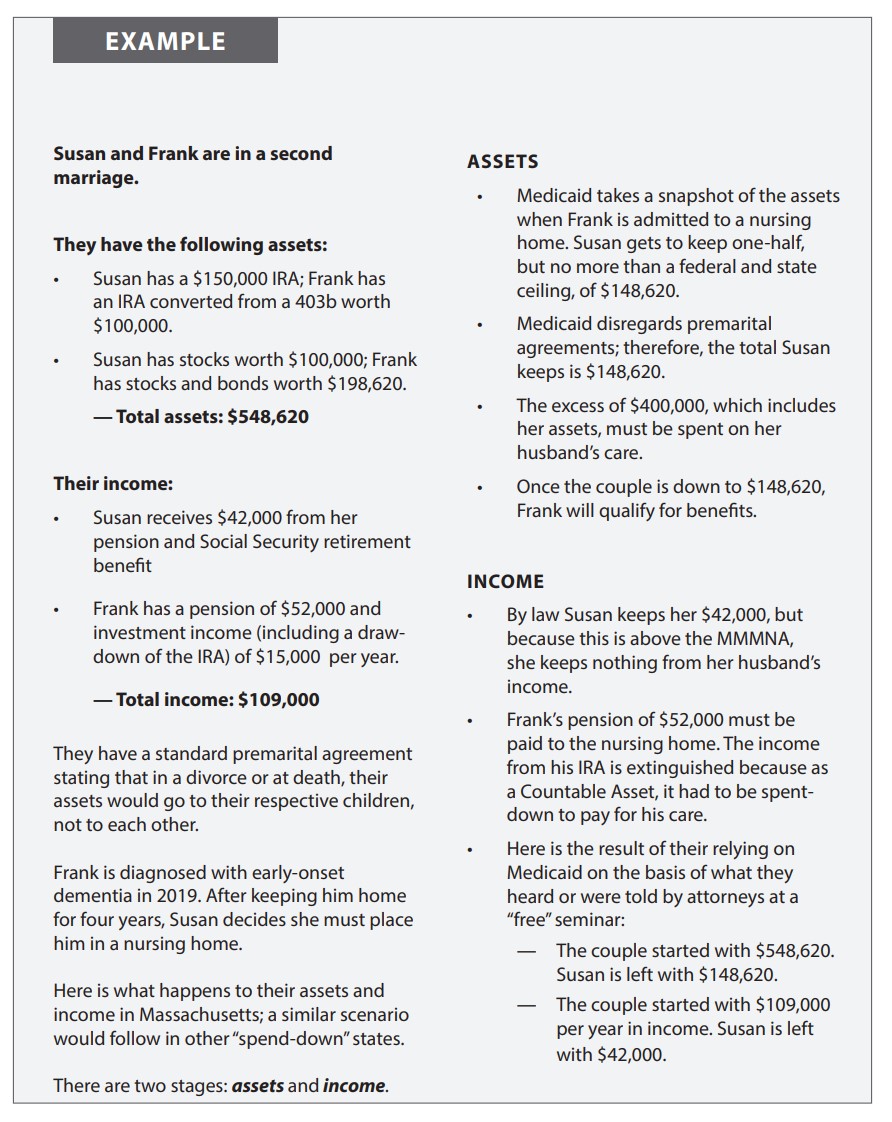

By the way, it does not matter if it’s a first, 2nd, or 3rd marriage, but the point is that Medicaid does not recognize prenup agreements in any state.

I’ve always believed that planning ahead for LTC is not something that we do for ourselves. It’s what we do for those we love – our spouses and our children. We want to protect them from being caregivers and totally upsetting their lives for as long as we may need care.

Isn’t it better for them to be our care “supervisors” and not our care “providers” to help keep us at home (where we all would rather receive the care and attention we deserve)?

Having a real plan (stress-tested) in place, whether it involves some insurance or not, protects the emotional, physical, and financial well-being of those we care most about as a consequence of our needing extended care at some point.

Nobody wants to contemplate needing “help” to get through the day. But if we live long enough, that might be possible, if not probable.

I just got back from visiting my 90-year-old Dad in his assisted living facility in South Carolina. I couldn’t even picture him in this position even 3 years ago. No, not at all.

In any case, to get a clearer idea of how Medicaid works (Medicare does not pay for LTC beyond 100 days — at best), look at the image below.

Susan is only allowed to keep the $148,000 or so, and they must spend down some $400,000 of Frank’s IRA before Medicaid pays for his care at a Skilled Nursing Facility.

MMMNA is the abbreviation for Minimum Monthly Maintenence Needs Allowance for the healthy spouse, which is about $2,300/month (before taxes), depending on the state.

Could you or your spouse live on that income level and support the lifestyle you’ve become accustomed to?

Of course, in this example, Susan’s income is well above that figure, so none of his income is protected for her.

CLICK on the image to make it clearer, and then hit your “back” button to return to the blog.

Medicaid is meant for the poor (or those who become poor via spending down of assets to qualify). The VA benefits (thank you for your service!) are limited with an eight-tier system to designate spots for limited beds (based on whether needing care was service-related and, of course, means testing).

In any case, if you want to receive care at home, neither of those programs offers very little, if any, programs for extended care at home.

To learn more about planning for extended care, Medicare, Medicaid, VA benefits, legal ploys such as Miller Trusts, insurance (both traditional LTC policies and the 20+ new types of LTC insurance plans), and more, check out my latest book about “Long-Term Care” by CLICKING this link.

all the best… Mark

PS – Although I started my financial services career in 1997 as an LTC specialist, a book reader asked me why I wasn’t a CLTC. So, despite being a CFP since 2000 and an RICP, I said I’d do it.

And I’ve got to admit that I’ve learned a few things about Medicaid and the VA benefits for those needing extended care. And when I update the book for 2024, I’ll make those additions.